Canada’s cannabis market is becoming easier to describe at a headline level and harder to understand at an operating level.

That is because the latest data points do not tell one simple story. They tell two stories that are both true at the same time.

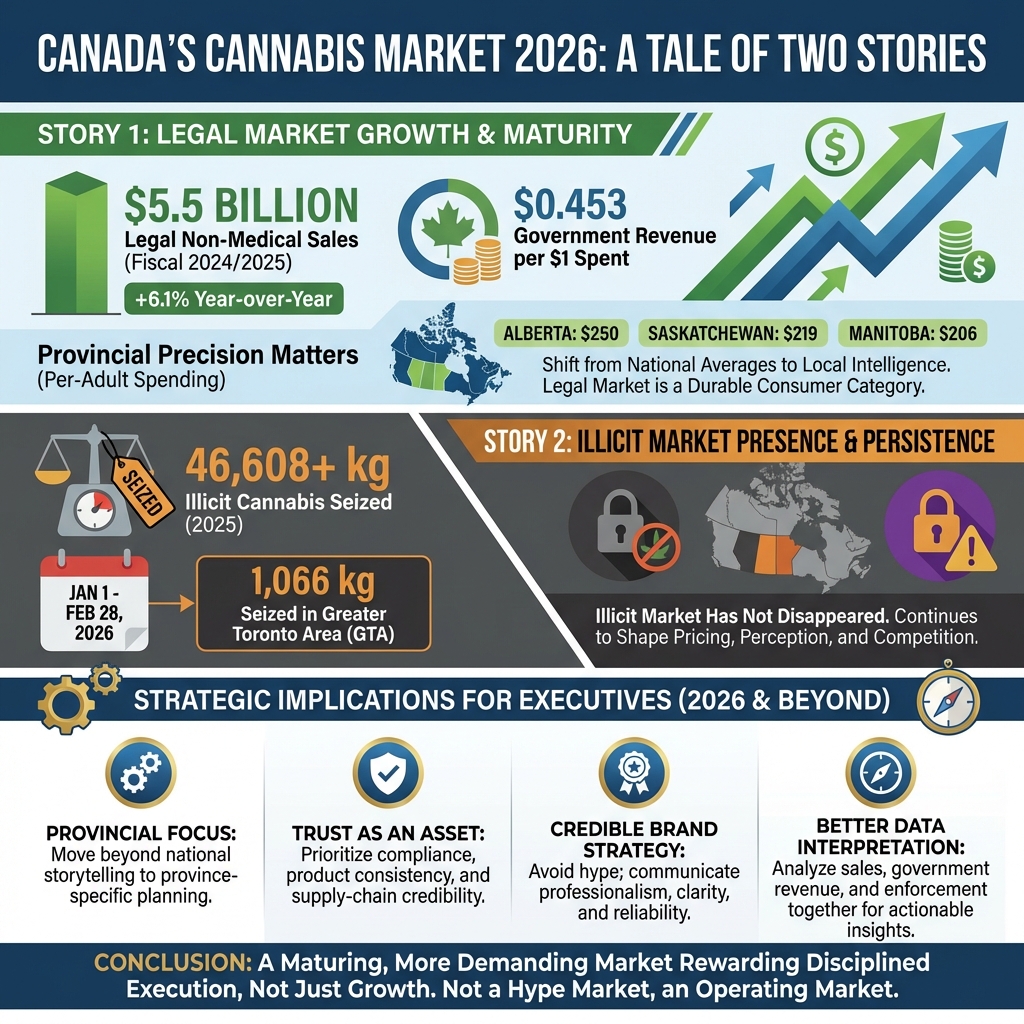

On March 5, 2026, Statistics Canada reported that legal, non-medical cannabis sales reached $5.5 billion in fiscal 2024/2025, up 6.1% year over year. The same release showed the market is now economically material at a provincial level: governments earned the equivalent of $0.453 for every $1 spent on cannabis, and the highest per-adult spending came from Alberta at $250, followed by Saskatchewan at $219 and Manitoba at $206.

One week later, on March 12, 2026, the Canada Border Services Agency reported that officers in the Greater Toronto Area had seized 1,066 kilograms of illegal cannabis between January 1 and February 28, 2026. The agency also stated it had seized more than 46,608 kilograms of illegal cannabis in 2025.

Read together, those two signals define the Canadian cannabis market in 2026. The legal market is larger, more stable, and more economically relevant than it was a few years ago. The illicit market has not disappeared, and its continued presence still shapes pricing, public perception, enforcement pressure, and competitive behaviour.

Why the latest Canadian cannabis market data matters

The legal side of the market is no longer a fragile proof of concept. At $5.5 billion in annual non-medical sales, cannabis has become a durable consumer category. Provinces have built retail infrastructure, consumers are purchasing through regulated channels, and governments now have a fiscal interest in the sector’s performance.

That is a meaningful shift from the early years of legalization, when the national conversation was dominated by store openings, shortages, oversupply headlines, and the question of whether the legal channel could ever meaningfully displace illicit supply.

Today, the answer is more nuanced. The legal market has achieved real scale. But scale is not the same thing as full market control.

That distinction matters because executives, investors, and policymakers often make mistakes when they assume legal-market growth automatically means structural pressure has gone away. It has not. In fact, the next phase of the Canadian cannabis industry may be defined by how well businesses perform inside a legal market that is stronger than before but still exposed to illicit distortion.

Provincial performance now matters more than national averages

One of the clearest lessons in the Statistics Canada release is that national growth alone is no longer enough to guide commercial strategy. The market is increasingly provincial in its real operating logic.

Alberta’s per-adult spending is not Quebec’s. Saskatchewan’s consumer behaviour does not look like Ontario’s. Retail density, product mix, distribution dynamics, consumer price sensitivity, and competitive intensity all vary by province. That means national averages are becoming less useful as a decision-making tool.

For licensed producers and brand leaders, this changes the planning model. In the next phase of Canadian cannabis, the strongest operators will not simply ask whether “Canada” is growing. They will ask where demand is most disciplined, where value is being captured, where their categories travel best, and where local competition makes their current strategy too generic to hold margin.

This is one of the clearest signs that the market is maturing. Mature markets punish lazy generalization. They reward segmentation, local intelligence, and sharper execution.

Why illicit pressure is still a strategic issue

The CBSA seizure numbers matter for more than enforcement headlines.

They remind the market that illicit supply remains commercially relevant, even if legal sales are growing. That continued illicit activity can still shape price expectations, pressure legitimate operators on value positioning, and reinforce the public perception that cannabis remains a high-friction category rather than a normalized regulated industry.

For businesses, that creates at least three practical implications.

First, trust becomes a commercial asset. When consumers, investors, or regulators continue to see evidence of illegal movement, licensed operators benefit from clearer positioning around product consistency, compliance discipline, and supply-chain credibility.

Second, brand strategy has to become more credible than theatrical. In a market where illicit supply remains active, hype-oriented positioning tends to age poorly. The brands that look durable are usually the ones that communicate professionalism, clarity, and reliability.

Third, data interpretation matters more. Sales growth, government revenue, and enforcement activity are not disconnected. Together, they tell leadership teams where pressure is building and where disciplined execution matters most.

What executives should do with the two-speed market reality

The most important implication for 2026 planning is that Canada’s cannabis market should now be understood as an operating market, not a hype market.

That shifts the strategic priority set.

Leadership teams should focus on:

- province-specific planning instead of national-average storytelling

- trust, compliance, and product clarity as part of competitive positioning

- stronger interpretation of public data into channel, pricing, and investment decisions

- realistic planning for a market where legal growth does not fully neutralize illicit pressure

This is also a boardroom issue. A business can now describe last quarter’s revenue performance and still misunderstand the deeper structure of the market it operates in. The better question is not only “did sales grow?” It is “what does current growth say about channel quality, risk concentration, pricing resilience, and the next move?”

FAQ: Canada cannabis market 2026

Is the Canadian cannabis market still growing?

Yes. Statistics Canada reported $5.5 billion in legal non-medical cannabis sales for fiscal 2024/2025, up 6.1% year over year.

Why does illicit cannabis still matter if legal sales are up?

Because persistent illicit activity still affects price competition, public perception, enforcement narratives, and how trust is built in the regulated channel.

What is the biggest strategy takeaway for cannabis operators in Canada?

National growth is no longer enough. Winning now depends more on provincial precision, disciplined positioning, and better interpretation of mixed market signals.

Why is this important for investors and advisors?

Because a large legal market can still be structurally stressed. Scale does not automatically mean margin stability, cleaner competition, or lower regulatory pressure.

Canada’s cannabis industry is not moving backward. It is moving into a more demanding phase. That is good news for serious operators and less comfortable news for anyone still relying on a simpler legalization-era narrative.